Scott Martorana

Risk Versus Return in M&A Transactions

Mergers and acquisition (M&A) transactions need to be looked at from a risk versus return perspective. Participants in deals, both the buyer and seller, should understand the value proposition of the transaction and determine whether it is better to continue to grow and thrive organically or execute on a deal. Understanding value drivers and how to optimize value is the key to prospering in the future.

Mergers and acquisition (M&A) transactions need to be looked at from a risk versus return perspective. Participants in deals, both the buyer and seller, should understand the value proposition of the transaction and determine whether it is better to continue to grow and thrive organically or execute on a deal. Understanding value drivers and how to optimize value is the key to prospering in the future.

1. Know your value and what drives it.

There are both value creators and value detractors that exist for every company. It might be weak internal controls, a consent order or a multimillion-dollar, unfunded pension that weakens your deal prospects. On the other hand, you may have strong core deposits, strong profitability metrics or an experienced and actively engaged management team with deep client relationships that drive growth and value.

Value detractors specific to each company can be corrected over time. As the risk profile of the company improves, it is shown that valuation multiples will also improve. A company that has many value detractors can improve its risk profile over time. By improving its risk profile, the company increases the market’s perception of the value of the company, leading to higher valuation multiples. As your institution’s comparative value to the market changes over time, you must conduct periodic valuations to understand what the company’s current value is and what is driving it.

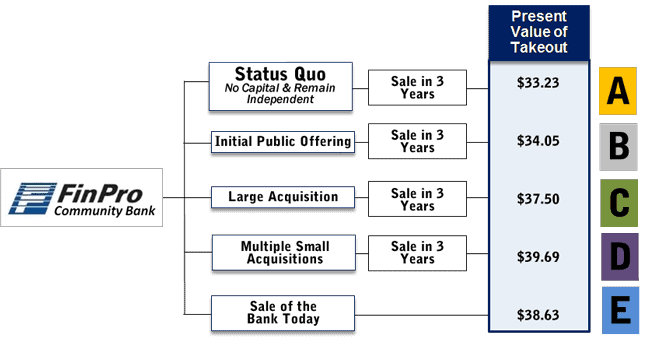

2. Understand your bank’s strategic paths, value and the execution risks of each path.

Once a company has a better understanding of its current value, it must understand the different decision tree paths available. Each of these paths will have a resultant present value of the company based upon executing on each path into the future. The risks and return associated with each path needs to be assessed. Below is an example of a strategic decision tree with five different paths. Each of these future strategic paths is modeled to determine the resultant present value resulting from each scenario path.

Not only is a present value calculated for each path, but the key risks and value drivers for each path need to be determined as well. For instance, if the company remains independent (path A), a key risk is that it may not be able to attract and retain key talent necessary for the company to thrive in the future.

In addition to the execution risks associated with each path, the financial value of the company under each scenario is also based upon a set of assumptions. Those assumptions must be reviewed carefully and the management team and the board of directors must critically review and sign off on those assumptions. More specific to M&A transactions, here are some of the major factors that impact an M&A deal:

- Price: A stronger buyer currency shortens the work-back period of tangible book value dilution in a stock transaction.

- Form of Consideration: Cash may decrease the work-back period of dilution in a transaction relative to utilizing stock consideration, due to higher earnings per share accretion, but utilizing cash will reduce the amount of capital at the combined entity.

- Cost Savings: Acquisition of smaller banks and in-market deals will generally have higher savings (30-50 percent), while market or business line expansions generally have somewhat lower savings (25-35 percent).

- Synergies: Deals can provide many synergies such as higher legal lending limit, greater franchise, new combined customer base, new sources of fee income, complementary loan and deposit products, or additional management bench depth for the combined entity.

- Transaction Expenses: These are nonrecurring expense items and therefore should not be included in the pro forma combined income statement going forward but will impact tangible book value per share (TBVS) dilution and work-back period. Transaction expenses should generally be 7-12 percent for community bank deals and levels outside the range should be reviewed.

- Mark-to-Market Assumptions: The target gets marked-to-market in a deal and these marks will initially impact TBVS upward or downward. The marks will be amortized/accreted through earnings over time. The marks generally have a bigger initial impact on TBVS and the earnings impact will be taken over a longer time period.

3. Recognize that a good deal on paper does not translate to a successful resultant entity.

Even with an extensive review of the assumptions, modeling and financial aspects of a transaction, a good deal on paper does not necessarily translate into a successful entity. Merger integration will make or break an institution’s ability to realize value in a transaction. Practical issues including vendor selection, branding and employee retention impact restructuring expenses. Social issues, such as corporate culture and leadership structure, define the bank moving forward.

Remember that there is an inherent risk versus return tradeoff in every M&A transaction. Understanding your institution’s risk profile, corporate culture, and all possible strategic paths will mitigate risk and maximize return.