Scott Gudmandson

The Window of Opportunity to Sell Is Now

Despite the recent pullback in bank stocks, valuations are still trading near a 10-year high (up 18.3 percent post-election). The drastic run up in both bank prices and trading multiples has had a direct impact on mergers and acquisitions (M&A) activity. The average price to tangible book value (P/TBV) for transactions is up 27 percent to 1.68 P/TBV since the presidential election. As multiples have expanded, buyers have a currency to pay higher values for targets in transactions. With bank valuations at a high level, both for publicly traded companies and their targets in an acquisition, management teams must evaluate two questions: Will the current optimism among bankers become reality? And, are we currently in a window of opportunity to sell?

Despite the recent pullback in bank stocks, valuations are still trading near a 10-year high (up 18.3 percent post-election). The drastic run up in both bank prices and trading multiples has had a direct impact on mergers and acquisitions (M&A) activity. The average price to tangible book value (P/TBV) for transactions is up 27 percent to 1.68 P/TBV since the presidential election. As multiples have expanded, buyers have a currency to pay higher values for targets in transactions. With bank valuations at a high level, both for publicly traded companies and their targets in an acquisition, management teams must evaluate two questions: Will the current optimism among bankers become reality? And, are we currently in a window of opportunity to sell?

To determine answers to these two questions we must first look into what is stoking investor optimism for bank stocks. There are three main drivers: rising interest rates and increased yields on loans, potential regulatory reform reducing associated noninterest expenses, and comprehensive tax reform reducing the overall tax burden on banks.

It would be overly optimistic to assume that all three of these factors would occur. Indeed, there are three main headwinds that should impede banks from increasing earnings to the most optimistic values: historical lessons, the current macroeconomic environment and government execution. These headwinds will not only have an impact on the trading of public bank stocks, but will have a direct impact on M&A pricing.

-

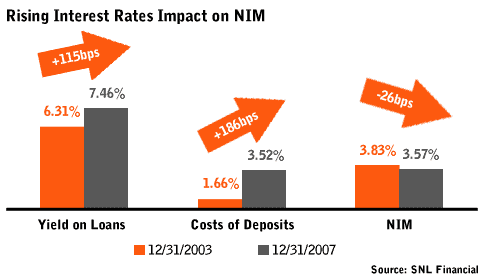

Historical lessons from a rising rate environment: From 2004 to 2006, rates increased from 100 basis points to 525 basis points. The thought has been that a rising rate environment will allow banks to increase earnings through higher yields on loans. However, from 2004 to 2006, we saw the exact opposite. As rates increased, deposits migrated to higher yielding products, offsetting the benefit from the increased yield on loans, ultimately leading to a decrease in net interest margin. As banks felt the pinch, they began to expand their balance sheets by increasing loan to deposit ratios. The years to come proved challenging as nonperforming assets increased drastically.

- Macroeconomic environment: Bull markets have historically lasted approximately seven years. We are more than eight years into the current bull-market run. How much longer can this bull-run last?

- Government execution: As the current trading multiples include regulatory and tax reforms that must be implemented by the government, we must ask ourselves if we can truly count on the government to deliver. Given the challenges the Republicans face passing healthcare reform, it is hard to believe that the Trump administration will be able to push through both comprehensive tax and regulatory reform without significant push back and concessions.

The headwinds facing the current optimism will have a direct impact on M&A pricing. If you are a potential seller and believe that the stars will align and all factors surrounding the current optimism will come to fruition, then enjoy the ride. If you are questioning any of these factors, it is likely that you have realized we are in a window of opportunity to sell.