Gerrit van de Wetering

Contingent Hedging Plans: How Community Banks Can Approach Hedging

Brought to you by BMO Capital Markets

Close

About the authors

Written by

Gerrit van de Wetering

A contingent hedging plan should be unique to every bank and developed in concert with internal modeling and management’s rate expectations. Like a captain adding ballast to a ship to provide a smoother ride, hedging allows a bank to reduce volatility and limit the impact of sudden interest rate changes. (See BMO’s previous article on this topic.) The goal is not to eliminate risk, but proactively mitigate or control risk at a suitable cost.

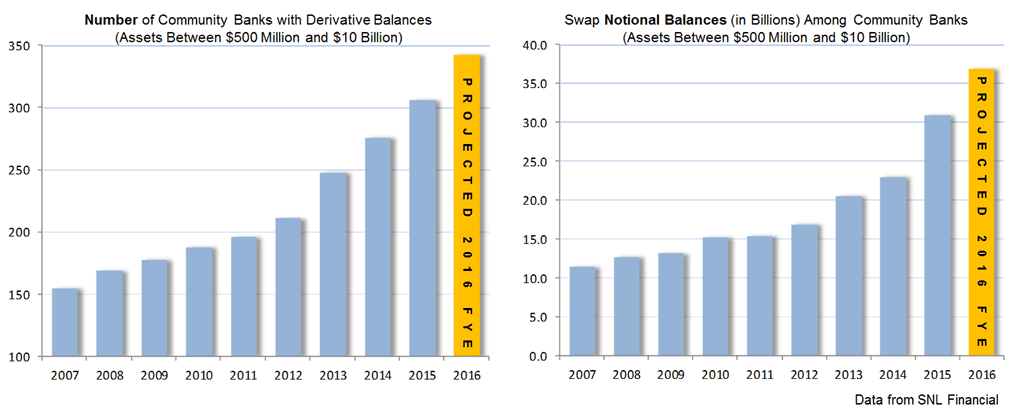

Derivative use among community banks has increased over the last several years. The graphs below illustrate the growth in the number of banks with swap and gross balances. Interestingly, after the Dodd Frank Act was enacted in 2012, at a time when using derivatives was expected to be more onerous, the year-over-year growth in derivative use among community banks has accelerated rather than declined.

One possible explanation with the migration of bankers from larger institutions to smaller community banks is they bring with them an understanding of derivatives and their benefits. The sustained flat curve and low rate environment may have compelled banks to evaluate and use derivatives.

How To Create a Contingent Hedging Plan

Regulators require banks to establish contingent funding plans. Developing a contingent hedging plan could follow the same approach. The plan can include description of roles, responsibilities and action plans where applicable. It should also allow management to act quickly when rate assumptions change. Among the items one can include:

Determine Economic Goals with Quantitative Guidance: What are the economic risks the bank is trying to mitigate? The more quantifiable the risk, the more specific you can be with your dealer and the more targeted the recommended solution.

List of Approved Transaction Types: Keep definitions broad enough to allow management to act opportunistically without waiting for approval at the monthly board meeting. Learn the basic mechanics of these trades today, so when you look to execute in a volatile market you will already have some understanding on which trades are most suitable for the risk.

Cost and Timing: There is usually a trade off or “cost” to do a hedge–nothing is for free. Get on someone’s rate sheet distribution, remain aware of current hedge levels and determine a range of acceptable cost. When one waits too long to trade, the hedge cost may become prohibitively expensive.

Understand Accounting Treatment: Derivatives are subject to FAS133 / ASC815 accounting treatment. Develop a familiarity of which accounting model is required and under which hedging circumstance.

Transaction Mechanics: Know who to call and how to execute a trade. Develop familiarity with terminology and swap nomenclature in order to accurately communicate intent.

Counterparty Selection: This may be the most important ingredient. Without access to a dealer counterparty to help provide solutions, creating a contingent hedging plan could be a moot point.

The Dodd-Frank Act provides advantages for hedgers if they transact with a registered swap dealer (RSD). The act defines swap dealers as entities who “hold themselves out as dealers in swaps; make a market in swaps; regularly enter into swaps with counterparties in the ordinary course of business for their own accounts; or engage in any activity causing the person to be commonly known in the trade as a dealer or market maker in swaps.”

These entities are required to register with the Commodity Futures Trading Commission and are held to higher business conduct standards. A list of provisionally registered swap dealers can be found here.

Hedgers Can Expect the Following Benefits From RSDs

Price transparency: The act requires all RSDs to quote mid + bid/offer spread on every trade. The hedger knows exactly what the dealer is making.

Liquidity / Cost: By trading directly with a market maker, the hedger crosses one bid or offer spread rather than two which normally happens when going through an intermediary.

Fair Credit Terms: You get fair credit terms with bi-lateral collateral posting for uncleared trades.

Expertise: RSDs can provide direct market color, trade recommendations and regulatory guidance. The level of expertise will be much higher given the critical mass and scale required to be a market maker in this regulatory environment.

Hedgers should consider that the regulatory burden on RSDs is significant, so dealers have responded by recalibrating business lines. While there are still RSDs willing to face small banks, many other dealers have exited the community bank space entirely. When evaluating a swap partner, you may want to ask about their commitment to your asset class.

WRITTEN BY