Rick Childs

Partner

Enter your email address and password below to gain access.

To login to the Online Training Series, please click here.

Rick Childs is a partner at Crowe LLP. He has over 35 years of experience in business valuation, transaction advisory services and accounting for financial services companies. Mr. Childs is the national practice leader overseeing the delivery of transaction and valuation services to the firm’s financial institutions clientele. His business valuation experience includes ASC 805 purchase price allocations including a focus on loan valuations, ASC 350 goodwill impairment testing and valuation of customer relationship intangible assets, including core deposit intangibles.

Mr. Childs is a frequent presenter for both national and state professional organizations including the SNL Financial, Bank Director, AICPA and Financial Managers Society. He has published articles on mergers and acquisitions in the ABA’s Commercial Insights, Community Banker, Bank Director and Bank Accounting & Finance.

The state of the bank merger and acquisition (M&A) market thus far in 2016 has been tepid compared to prior years. 2015 began the same way, but was helped by a tremendous fourth quarter in which the number of deals announced was more than 25 percent higher than the average of the first three quarters of the year. At the end of 2015, many bankers and industry experts hoped that the euphoria from the fourth quarter would carry over into 2016. Instead, the first quarter of 2016 saw M&A deals retreat to the moderate levels experienced in the first three quarters of 2015, with a modest increase in the second quarter giving way to a much lower third quarter. Year-to-date, announced deals are down a modest 5.6 percent compared to the same time period last year.

M&A Activity by Region

| Quarter | Mid Atlantic | Midwest | Northeast | Southeast | Southwest | West | Other* | Total Deals |

| 2015-Q1 | 7 | 26 | 2 | 12 | 10 | 8 | 65 | |

| 2015-Q2 | 5 | 27 | 5 | 14 | 11 | 7 | 69 | |

| 2015-Q3 | 9 | 24 | 3 | 9 | 12 | 6 | 1 | 64 |

| 2015-Q4 | 13 | 30 | 3 | 24 | 6 | 7 | 83 | |

| 2016-Q1 | 4 | 38 | 1 | 10 | 5 | 5 | 1 | 63 |

| 2016-Q2 | 6 | 29 | 2 | 14 | 7 | 8 | 66 | |

| 2016-Q3 | 4 | 25 | 1 | 14 | 6 | 7 | 57 |

*No geography listed

Source: SNL Financial, an offering of S&P Global Market Intelligence

The Midwest has been bolstering the modest numbers experienced year-to-date. This impact on the overall percent change in M&A activity for 2015 and the first three quarters of 2016 is apparent when compared to the other regions.

Indicators Affecting Bank M&A

Oil prices have had an impact on the number of deals in the Southwest. Credit quality does have an impact on deal volume, but between Jan. 1, 2015, and June 30, 2016, credit quality has been fairly good compared to the levels experienced in years 2008 to 2010.

The decline in longer-term interest rates could have an impact on buyers’ perceptions of banks’ future earnings prospects with already compressed net interest margins. The 10-year U.S. Treasury constant maturity rate has flattened in 2016, and this could be a contributing factor in the number of announced bank M&A deals.

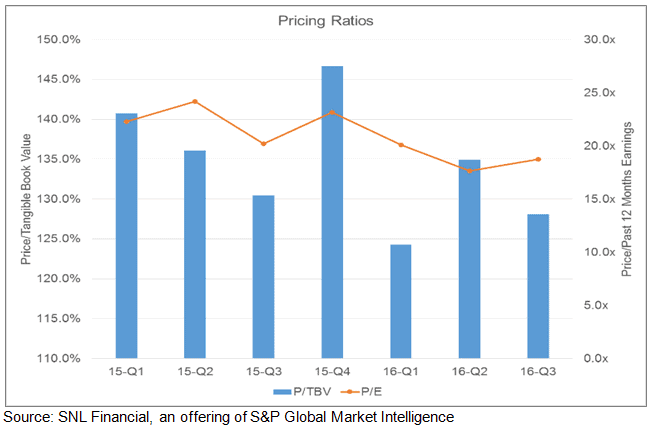

As shown below, average deal pricing has declined, which also could be contributing to the decline in the number of M&A deals announced.

Pricing Over Time

Although not shown, a review of the trailing 12-month return on assets for the selling banks and also the level of tangible equity and tangible assets shows they are fairly consistent quarter to quarter, so these financial metrics are not responsible for the decline in either pricing ration.

An overrepresentation of the banks in the Midwest also has had an impact on why the median pricing ratios have declined. The sellers in this region tended to be smaller, and the size of the seller does affect the price realized:

Median Price/Tangible Book Value Jan. 1, 2015, through Sept. 30, 2016

| Asset Size of Seller | Mid Atlantic | Midwest | Northeast | Southeast | Southwest | West | Total |

| <$50 Million | N/A | 121.9% | NA | 96.9% | 115.3% | 50.1% | 115.3% |

| $50M – $100M | 129.1% | 108.4% | 146.7% | 96.3% | 132.7% | 128.1% | 114.4% |

| $100M – $500M | 122.6% | 126.2% | 142.6% | 136.2% | 150.1% | 133.5% | 133.3% |

| $500M – $1B | 161.5% | 136.0% | 125.7% | 161.4% | 165.8% | 178.7% | 157.7% |

| $1B – $5B | 152.8% | 179.3% | 164.2% | 194.9% | 156.9% | 222.1% | 179.3% |

| $5B – $15B | 219.4% | 155.7% | N/A | 233.0% | N/A | N/A | 219.4% |

| >$15B | 159.8% | 199.3% | N/A | 151.5% | N/A | 272.1% | 171.4% |

More than 80 percent of the transactions announced involve sellers with less than $500 million in assets, which explains the lower realized pricing ratios. The Midwest contains a significant number of bank charters with less than $500 million in assets and, as a result, if this region’s total deal volume is up and the rest of the regions are down or flat, the impact on the overall pricing still will trend down.

Looking Ahead

The big questions remaining are what will happen in the fourth quarter of 2016 and whether the industry’s experience this year will be a predictor for 2017.

None of the economic factors are expected to materially improve for the fourth quarter. The Federal Reserve is expected to increase interest rates modestly, but there are Fed governors who favor no interest rate increase this year. As a result, it appears unlikely that the compression of net interest margin will improve drastically over the next 15 months. What does seem likely to occur is consistent quarter-to-quarter deal totals, although a reduction in the number of deals in the Midwest region could lead to even lower M&A totals for 2017.

Rick Childs is a partner at Crowe LLP. He has over 35 years of experience in business valuation, transaction advisory services and accounting for financial services companies. Mr. Childs is the national practice leader overseeing the delivery of transaction and valuation services to the firm’s financial institutions clientele. His business valuation experience includes ASC 805 purchase price allocations including a focus on loan valuations, ASC 350 goodwill impairment testing and valuation of customer relationship intangible assets, including core deposit intangibles.

Mr. Childs is a frequent presenter for both national and state professional organizations including the SNL Financial, Bank Director, AICPA and Financial Managers Society. He has published articles on mergers and acquisitions in the ABA’s Commercial Insights, Community Banker, Bank Director and Bank Accounting & Finance.