Well-documented stories of speculators using derivative structures to gamble and lose their firms’ capital, along with Warren Buffett tagging them as “financial weapons of mass destruction” have made interest rate swaps a non-starter for many community banks. It seems that the preponderance of evidence against derivatives has led many community bank boards to view the issue as an open and shut case, rather than carefully considering all of the facts before passing judgment on these instruments. But questioning the four most common objections to swaps uncovers some overlooked truths that may motivate your board to take a fresh look at derivatives.

Well-documented stories of speculators using derivative structures to gamble and lose their firms’ capital, along with Warren Buffett tagging them as “financial weapons of mass destruction” have made interest rate swaps a non-starter for many community banks. It seems that the preponderance of evidence against derivatives has led many community bank boards to view the issue as an open and shut case, rather than carefully considering all of the facts before passing judgment on these instruments. But questioning the four most common objections to swaps uncovers some overlooked truths that may motivate your board to take a fresh look at derivatives.

1. I know someone who lost money on a swap…but why?

Putting aside situations where derivatives were sold inappropriately, the claim, “I know a customer who got burned using a swap,’’ is simply the banker stating that the borrower utilized an interest rate swap to lock in borrowing costs. A borrower who chose the certainty offered by a swap over uncertain variable interest payments ultimately paid more because interest rates went down instead of up, and then stayed low. In reality, the borrower was burned by the falling rate environment while the interest rate swap performed exactly as advertised, providing known debt service, albeit higher than the prevailing rates. It looked like a bad deal only with 20-20 hindsight.

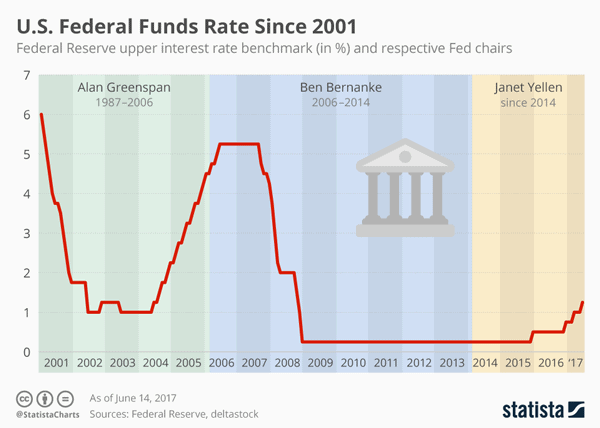

With the Federal Reserve now moving short-term rates higher while market yields remain close to historic lows, the odds begin to favor the borrower who uses a swap to hedge against rising rates. Whether or not the swap pays off, the certainty that it delivers becomes more attractive as rates become volatile and their future path remains uncertain.

2. Regulators don’t want community banks using swaps…or do they?

When looking at the topic of interest rate risk, regulators began sounding alarm bells for banks in the years following the crisis on the premise that there was nowhere to go but up for rates. In a 2013 letter to constituents, the Federal Deposit Insurance Corp. (FDIC) re-emphasized the importance of prudent interest rate risk oversight and issued this warning:

“Boards of directors and management are strongly encouraged to analyze exposure to interest rate volatility and take action as necessary to mitigate potential financial risk.”

When it came to outlining mitigation strategies in this letter, rather than banning derivatives as intrinsically risky, the FDIC specifically mentioned hedging as a viable option. They did, however, sound a note of caution:

“…institutions should not undertake derivative-based hedging unless the board of directors and senior management fully understand these instruments and their potential risks [emphasis our own].”

Compared with other risk management tactics, derivatives offer superior agility and capital efficiency along with new avenues to reduce funding costs. Accordingly, it may behoove banks to heed the FDIC’s exhortation and implement derivatives education for directors and senior management.

3. My peers don’t use swaps…why should I?

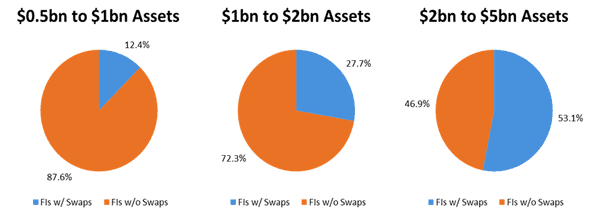

If you are not hedging with swaps and your total assets are between $500 million and $1 billion then you are in good company; seven out of eight banks your size have also avoided their use. But if your growth plans anticipate crossing the $1 billion asset level, more than one in four of your new peers will be using swaps. Once you cross the $2 billion mark more than half of your peers will be managing interest rate risk with derivatives, while institutions not using swaps become a shrinking minority. For the many institutions serving small communities and not expecting to cross the $500 million asset level in the foreseeable future, derivatives are not typically a viable solution. But if your growth will soon push you into a new group of peers with more than $2 billion in assets on the balance sheet, then having interest rate swaps in the risk management tool kit will become the norm among your competitors.

4. Our board doesn’t need derivatives education…or do we?

After digging below the surface we learn that most of the instances where derivatives left a bad aftertaste were caused by an unexpected drop in rates rather than a product flaw. We also learn that in urging banks to take action to mitigate interest rate risk, the regulators are not anti-derivative per se; they simply lay out the reasonable expectation that the board and senior management must fully understand the strategy before executing. Taking the time to educate your board on the true risks as well as the many benefits provided by interest rate hedging products may help to distinguish them as powerful tools rather than dangerous weapons.