Lucas Parris, senior vice president, is the leader of Mercer Capital’s Financial Reporting Valuation Group, providing public and private clients with fair value opinions and related assistance pertaining to goodwill and other intangible assets, purchase price allocation, stock-based compensation, and illiquid financial assets.

Lucas also leads Mercer Capital’s Insurance Industry Team, specializing in valuation and advisory services for insurance agencies, brokerages, underwriters, third-party administrators, and other industry service providers. These services include independent valuations for corporate transactions, agency perpetuation, buy-sell agreements, financial reporting, tax compliance, and buy or sell side consulting services.

Lucas Parris

Senior Vice President

SHARE THIS ARTICLE

A decade ago, interest rates were near zero, the S&P 500 was close to 1,600 and Bitcoin finished the year at a mere $300.

The narrative at that time was that the lingering effects of the great recession, higher capital requirements for banks and frothy valuations for insurance agencies (driven by private equity bidders) had firmly crowded banks out of the market for buying insurance businesses.

Over the last 10 years, a few banks invested in their insurance agency operations, though mostly for organic growth. At the same time, market multiples and private equity’s appetite for agencies only increased, leading to some very favorable outcomes for banks willing to sell those businesses.

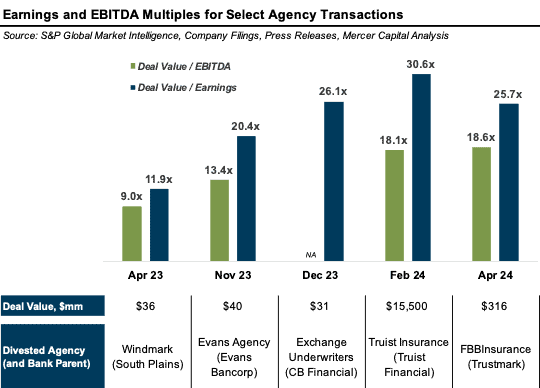

Sellers in recent months have included Truist Financial Corp. in Charlotte, North Carolina; Trustmark Corp. in Jackson, Mississippi; and BOK Financial Corp. in Tulsa, Oklahoma.

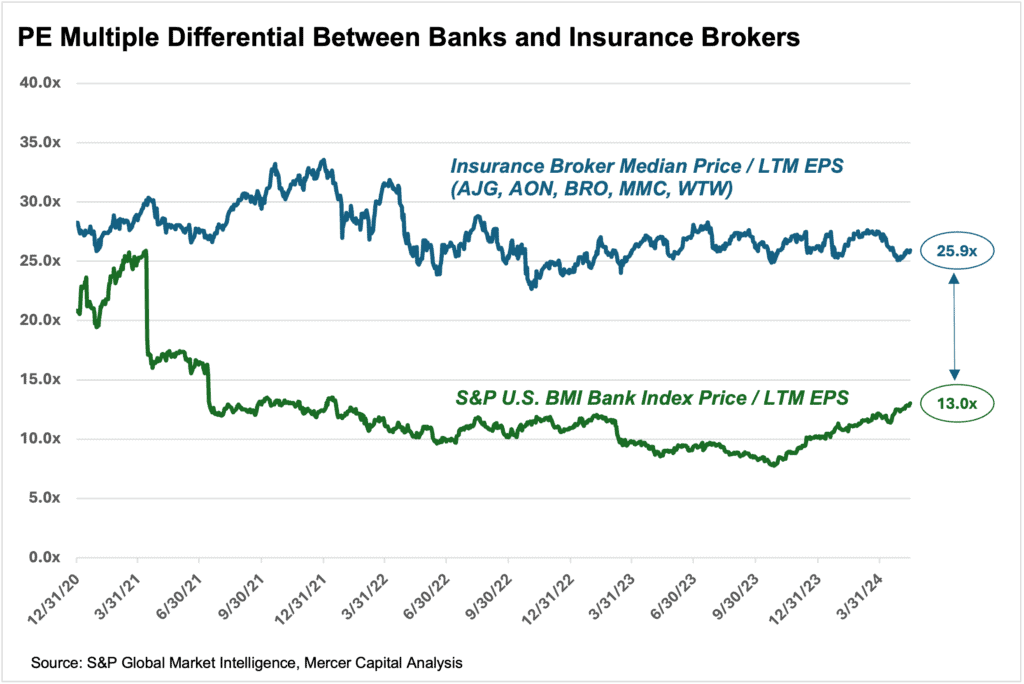

How did we get to this point? What is the next step in this cycle? The differential between PE multiples for banks and insurance brokers has been widening for several years, due in part to market dynamics and interest rates. That has led to lower returns (and expectations) for banks compared to public insurance brokers.

So, it would make sense for banks with significant insurance operations to wonder if the value realization of a dollar of insurance income would be better captured outside the bank’s typical pricing multiples.

This arbitrage of earnings multiples has undoubtedly influenced many sellers of bank-owned agencies. As observed by S&P Global Market Intelligence, 2023 was the first time in at least eight years that U.S. banks sold more insurance agencies than they acquired.

The strategic rationale for the latest group of divestitures has been largely consistent. Capitalizing on the sale of an insurance unit at a favorable valuation provides several potential benefits, including:

1. Allowing for capital redeployment from lower-yielding to higher-yielding securities;

2. Offsetting losses from a securities portfolio repositioning.

3. Enhancing capital ratios.

4. Creating tangible book value per share accretion.

5. Providing more support and focus for the core banking business.

In certain circumstances, the driving force behind a transaction might be the strategic imperative of a particular acquirer, such as the desire to bolster presence in a geographic market or to double down on a particular line of business. It is worth noting that the price paid as a multiple of insurance revenue is only loosely correlated with size. Margins and strategic considerations factor more prominently into earnings and EBITDA multiples.

Are bank acquisitions of insurance agencies a thing of the past? Not necessarily. Hindsight is always 20/20. Perhaps banks should have pushed back against the private equity buyers over the last decade and been willing to bid higher on deals. In retrospect, paying up to 12x EBITDA for a small insurance agency doesn’t seem that crazy when the consolidated unit can now be monetized at 15x.

Often, the best determinant of total return in an acquisition is the entry price. If a bank has the ability to source proprietary off-market agencies or books of business through local connections, that strategy is still well worth considering.

What about banks that already have an insurance unit? What steps should they take? Here are a few suggestions:

Conduct a strategic evaluation of the agency in the context of the overall strategy. Does the agency fit into long-term vision? Is the sum of the parts greater than the whole?

What is the agency’s true earning power or valuation on its own? Consider obtaining an independent valuation or quality of earnings study to analyze the financials, ask the difficult questions, and examine the business in the way that a potential acquirer would.

Is the business ready for sale? Is the corporate structure clean or messy? Do you have a collection of third-party producer arrangements that must be consolidated? Are there minority owners? How does the expense allocation and/or resource sharing between the bank and agency work?

Do you have alignment between the agency and bank management? Are there separate boards? Intertwined management and/or ownership? Would a sale create potential issues of conflict or necessitate a fairness opinion?

The overarching question to answer is whether selling a business that took 20 years to build is the right long-term move. Maybe. Is it shortsighted to sell off a golden goose agency in the name of “balance sheet repositioning?” Maybe not. Each situation and transaction is unique. Clearly, the banking and insurance industries are at an interesting place right now and if you are a participant in both, then you have a few options to consider.

WRITTEN BY

Lucas Parris

Senior Vice President

Lucas Parris, senior vice president, is the leader of Mercer Capital’s Financial Reporting Valuation Group, providing public and private clients with fair value opinions and related assistance pertaining to goodwill and other intangible assets, purchase price allocation, stock-based compensation, and illiquid financial assets.

Lucas also leads Mercer Capital’s Insurance Industry Team, specializing in valuation and advisory services for insurance agencies, brokerages, underwriters, third-party administrators, and other industry service providers. These services include independent valuations for corporate transactions, agency perpetuation, buy-sell agreements, financial reporting, tax compliance, and buy or sell side consulting services.