Krista Morgan

Leveraging Fintechs to Do More with Less

Close

About the authors

Written by

Krista Morgan

Fintech is often viewed as a disrupter to the banking industry, but it greatest influence may be as a collaborator.

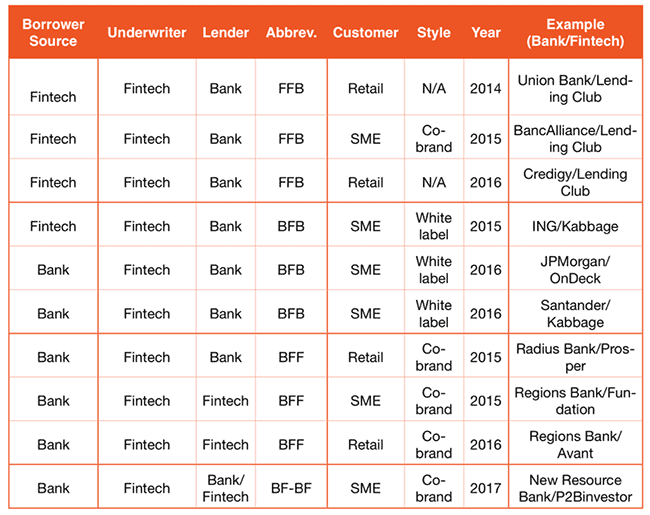

Financial technology companies, often called fintechs, can provide benefits both banks and themselves, especially when it comes to lending. But banks need to be prepared for the potential challenges that can arise when forming and executing these partnerships.

Partnerships between community banks and fintechs makes sense. For community banks, the cost of building or buying their own online loan origination platform can be prohibitive. A partnership with a fintech can help banks achieve more with less risk.

Banks can partner with fintechs to improve services at a significantly lower capital expenditure, reducing the cost of doing business and reaching market segments that would otherwise not meet their credit criteria. Collectively, these relationships advance not only the business of community banks, but also their mission.

Partnering with banks offers fintech firms brand exposure, allows them to more quickly scale their business and increases their access to capital and liquidity, which can translate to better company returns.

Community banks and fintech firms should be natural allies, given the market dynamics and growth in online lending, the underfunding of small businesses and the increased competition facing smaller institutions.

Community banks are also ideal first movers in the bank-fintech partnership space, given the personal nature of the business, low cost of capital and ability to move quicker than regional banks. Community banks are the preferred source of funding for small- and medium-sized enterprises, and consistently receive high marks from clients for customer service and overall experience.

However, there can be challenges. Bank respondents cited their firms’ overall preparedness as a point of concern when considering a fintech collaboration, according to a recent paper on bank-fintech partnerships from law and professional services firm Manatt. The Office of the Comptroller of the Currency and Consumer Financial Protection Bureau mandate that banks must implement appropriate oversight and risk management processes for third-party relationships and service providers.

Other issues that could arise for community banks when pursuing a fintech partnership include data security, staff training and technology integration with legacy systems. It’s imperative that community banks are clear about the responsibilities, requirements and protections that will contribute toward a successful partnership in conversations with a fintech firm.

Despite their desire to fund local businesses, community banks sometimes encounter significant pressures that prevent them from doing so. These issues are amplified by various market forces and longstanding structural inefficiencies such as consolidation, slower economic expansion, increased regulation and more-stringent credit requirements. Consumer expectations around new channels and banking services compound the situation. Community banks need to adapt to this new dynamic and complex ecosystem. Without a strategy that includes technological vision, banks risk becoming irrelevant to the communities they serve.

Fintech firms – reputed as industry disruptors – can be powerful collaborators and allies in this land grab. They can help banks expand their borrower market by reaching customers with alternative credit profiles and providing technology-driven improvements that enhance the customer experience. The inherent advantages held by community banks make them well positioned to not only capitalize on these opportunities, but to lead the next wave of fintech innovation.

WRITTEN BY